The Financing Process

Demystifying Home Loans

The home loan process can feel overwhelming. By collaborating with a trusted lender and remaining informed through every step of the process, from pre-approval to closing, you can have a significantly more comfortable experience. You’ll want to consult with a mortgage specialist (or two) to find a professional who you are confident will provide you with the best care.

To get an idea of what to expect, review the following home loan process steps.

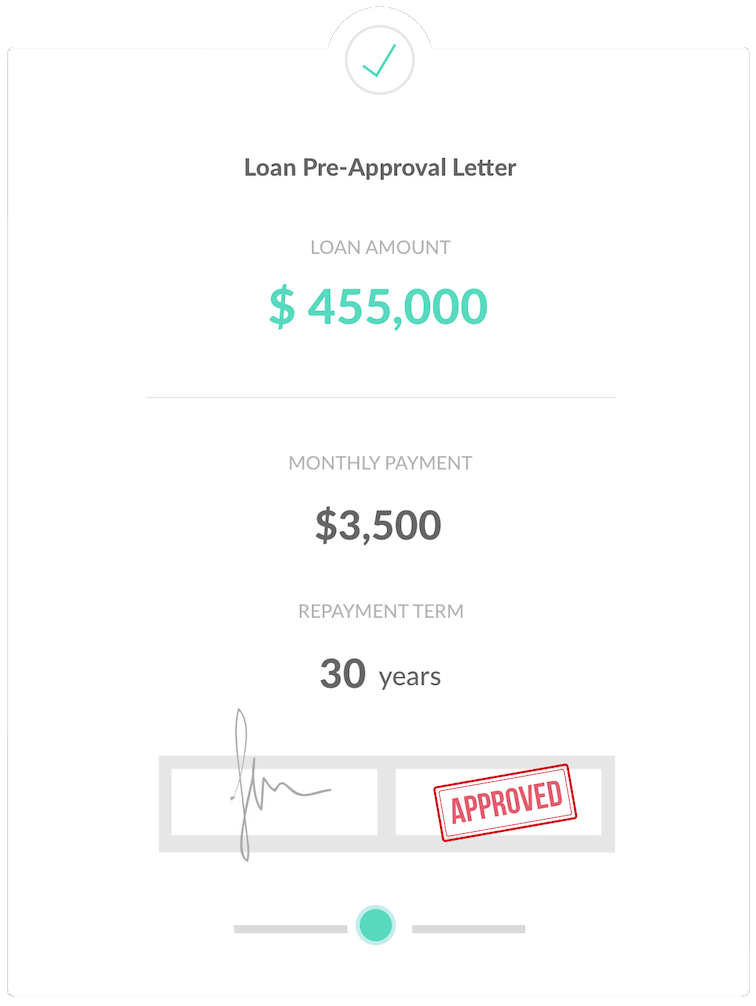

Step One:

Get Pre-Approval

Before you begin your home search, it’s a smart and proactive step to meet with a lender and get pre-approved for a loan amount. Offers that include a pre-approval letter are stronger and stand out — especially in competitive situations where sellers may be reviewing multiple offers.

To obtain pre-approval, your chosen lender will review your income, assets, and debts to determine how much you can comfortably borrow. This process typically includes a credit report, W-2 forms, pay stubs, federal tax returns, and recent bank statements.

There are many types of home loan programs available, each offering different benefits depending on your financial goals and preferences. Your lender can explain the details of each option to help you choose the loan program that best fits your needs.

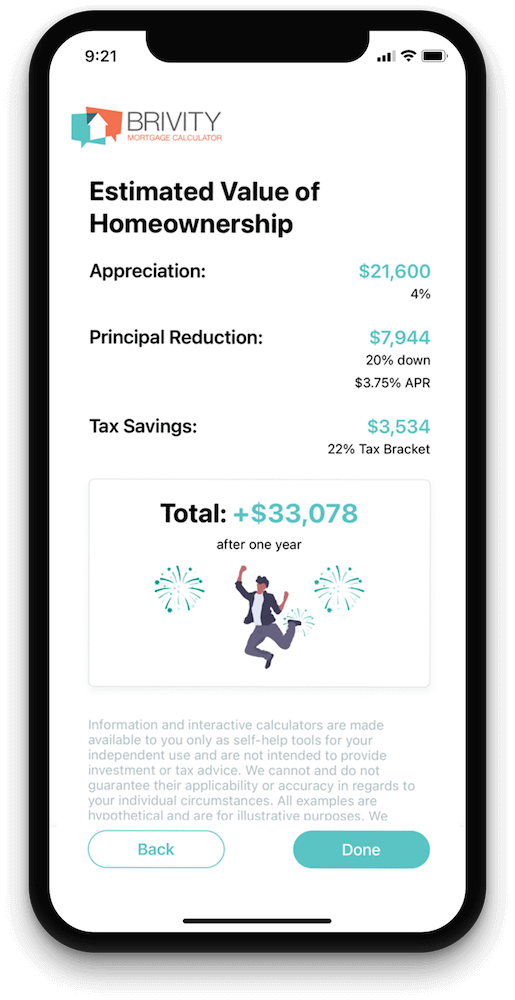

Estimate Your Monthly Payment

Estimate your mortgage payment, including the principal and interest, taxes, insurance, HOA, and Private Mortgage Insurance.

Price

Annual Tax

Loan Term (Years)

Down Payment %

Interest Rate %

Monthly HOA

Monthly Insurance

$3,198.20

Estimated Monthly Payment

Principal

$2,398.20

(75.0%)Taxes

$500.00

(15.6%)Private Mortgage Insurance (PMI)

$0.00

(0.0%)HOA

$100.00

(3.1%)Insurance

$200.00

(6.3%)

Step Two:

Find the best loan

Collaborating with a top-notch local loan officer will ensure you have access to competitive rates and programs that best fit your individual needs. Take the first step by completing this form to get connected today!

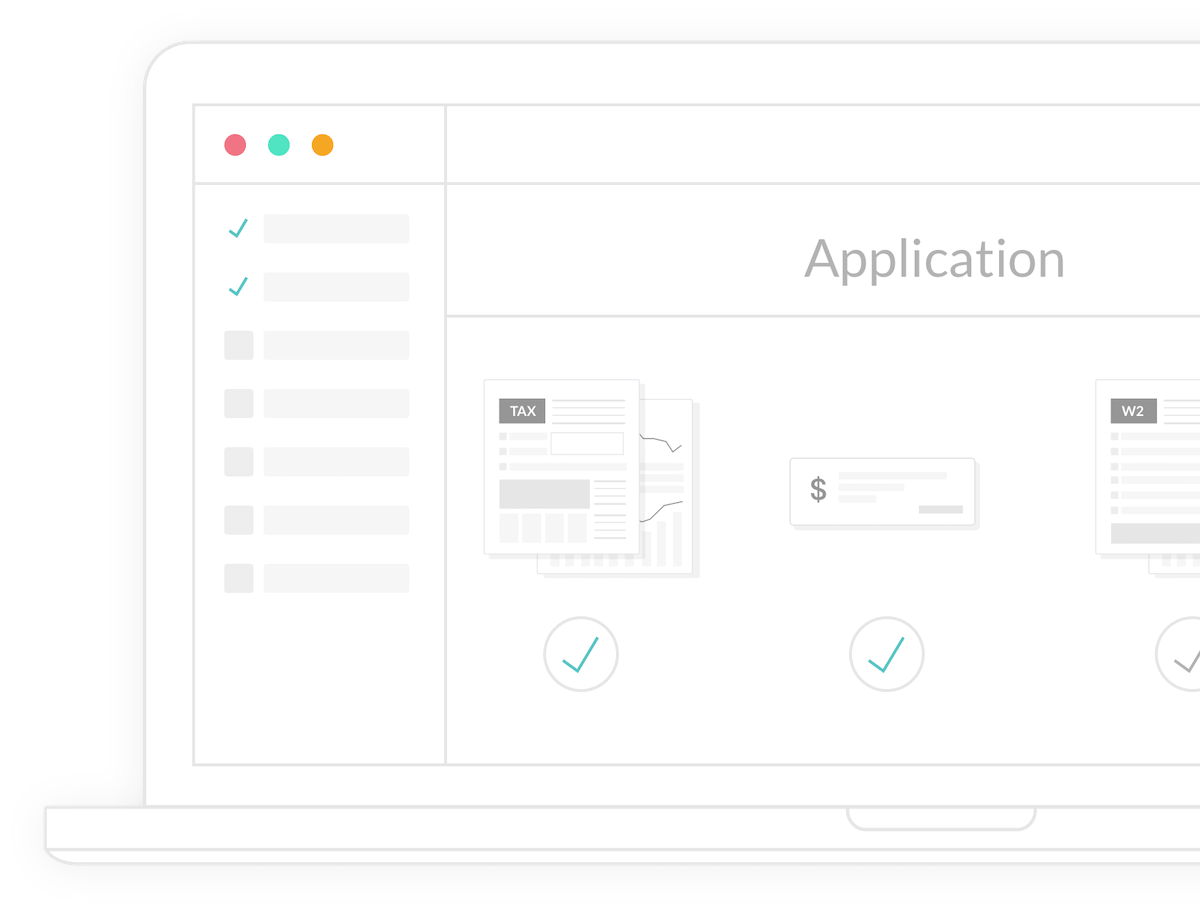

Step Three:

Application and processing

Once you’ve found the perfect property and your offer is accepted, your lender will guide you through completing a full mortgage loan application, reviewing down payment options, and explaining any related fees.

After your application is submitted for processing, your lender’s team will carefully review all documentation and order both a home appraisal and a property title search.

Next, your loan file is sent to underwriting, where an underwriter evaluates the complete package to ensure it meets all lending and compliance requirements. It’s common for your lender to request additional documentation or clarification during this stage — a normal part of ensuring a smooth approval process.

Step Four:

Final Steps to Homeownership

Once your loan is approved, you’ll need to secure homeowners insurance.

Your documents will then be sent to the title company, and a closing date will be scheduled for you to sign the necessary paperwork and pay any remaining costs to complete your home purchase.

After the loan goes through the required recording process, the purchase is complete — and you officially own your new home!